How to choose a lender?

Gone the days of past where there were hundreds of loan programs, and anyone could qualify for a loan on the spot! Now, everyone can qualify for a loan, it just may not be right now, and there may be certain qualification criteria you may have to meet in terms of credit, income, assets, or home equity.

With a competitive real estate seller’s market in 2023 for Metro-Detroit, it is critical that you use:

- Local Lender – a lender that is familiar with the area and has a great reputation for getting the job done. Rate shopping just isn’t as common, and there really isn’t a very wide variation in rates, however structuring the loan that works best for you is what will set an experienced lender apart from the rest

- Lender and Real Estate Agent Team – I personally had 3-4 lenders that I use on a regular basis. Some of the lender loan programs will vary slightly, and some have some unique programs, but overall, it’s also about getting the job done. Using one of the lenders I recommend is also a crucial step in getting your offer accepted on a purchase. I cannot promote the lender with your offer, or anticipate a closing date if I’ve never worked with them before.

Here are some of the unique strategies that we are advising clients so they can make a smooth transition to their first home or next home.

What’s the most common home loan options in Michigan?

There are several common home loan purchase programs available to homebuyers. Here are some of the most popular ones:

- Conventional Loans: Conventional loans are mortgage loans offered by private lenders and not backed by a government agency. They typically require a higher credit score and a larger down payment compared to government-backed loans. Conventional loans offer a variety of options, including fixed-rate and adjustable-rate mortgages.

- FHA Loans: The Federal Housing Administration (FHA) offers FHA loans, which are government-backed mortgages. These loans are designed to make homeownership more accessible, particularly for first-time buyers. FHA loans have more lenient credit requirements and lower down payment options (as low as 3.5% of the purchase price).

- VA Loans: VA loans are available to eligible military service members, veterans, and their spouses. They are guaranteed by the U.S. Department of Veterans Affairs and offer favorable terms, including no down payment requirement and competitive interest rates.

- USDA Loans: The U.S. Department of Agriculture (USDA) offers USDA loans for eligible homebuyers in rural and suburban areas. These loans are designed to promote homeownership in these areas and often come with low or no down payment options.

- MSHDA – Michigan State Housing and Development Authority (MSHDA) has loan programs, home buyer down payment assistance, as well as hardship programs.

It’s important to note that the availability of these programs and their terms may vary based on factors such as your location, income, credit history, and the specific lender you work with. It’s advisable to consult with a mortgage professional or research the options available in your area to determine which home loan purchase program is the best fit for your needs.

Unique Loan Options:

Down Payment Assistance – These programs primarily benefit first time homebuyers, or if you haven’t owned a home in the last 3 years. An experienced lender will evaluate your situation, and may figure out if you qualify for one of these programs. For instance, in some situations, a divorce will reset the first time homebuyer criteria. Most common Down Payment Assistance programs in Michigan are National Faith Home Buyer, and MSHDA. Some local lenders also have their own programs. For more information, visit the page specifically for Down Payment Assistance here.

Home Equity Line of Credit (HELOC) – Beat the competition by offering Cash on your next move!! In some situations where a homeowner has equity, we’ve successfully utilized one of my lenders to use a Home Equity Loan, and pay cash for your next home. Once the purchase is finalized, usually the homeowner sells the original house and everything is paid off. Cash is king and will usually always beat a financing offer.

Bridge Loan – A bridge loan is a type of short-term financing option that can be used to purchase a home when you haven’t yet sold your existing home or don’t have access to sufficient funds for the down payment. It acts as a “bridge” between the purchase of your new home and the sale of your current one, providing you with temporary funds to cover the gap.

When you’re in a situation where you’re buying a new home but haven’t sold your existing one, a bridge loan can help you secure the new property without having to wait for the sale to close. It essentially “bridges” the financial gap between the purchase of the new home and the receipt of funds from selling your current home.

Loan Reforecasting – This is where the you take the proceeds from the sale of your home and put them towards the down payment of your next home after you have already purchased. Rate, and term stays the same, but your loan amounts are “Reforecasted”

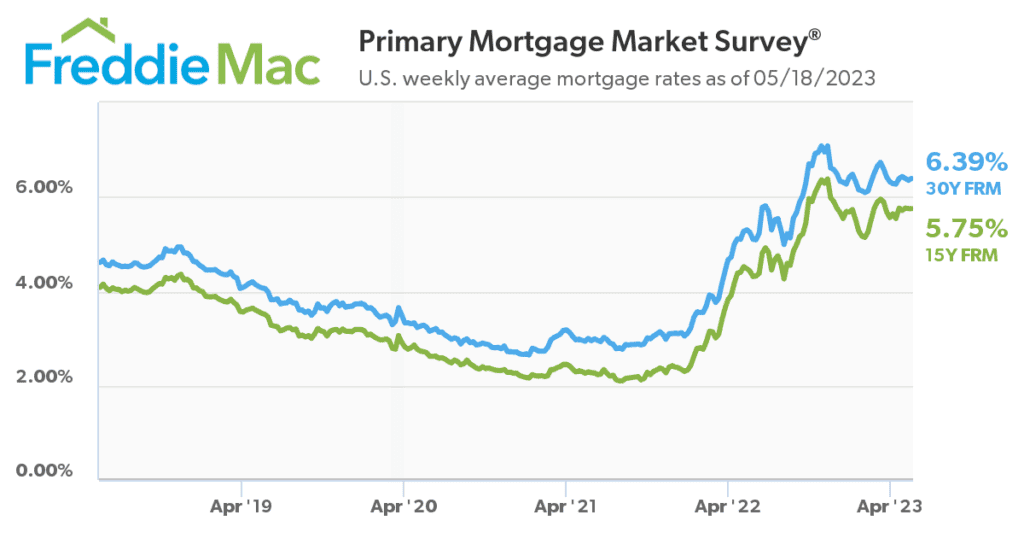

Loan Assumption – This is usually a fairly rare situation, but is possible. Home loan purchase rates started trending downwards toward the end of 2018 and rising at the beginning of 2022. This 4 year period had extremely low interest rates. (See photo below)

If you are purchasing a home, we can analyze the current loan and see if it’s assumable. The benefit of an assumption, is that you not only can benefit from a great interest rate, but you also will have less remaining payments, as well as more of your payment amount applied to principal than a starting loan.

Need an experienced Lender Referral?

I work with several lenders depending on your situation, and if you have an specific criteria that would be better for you to go with one lender over the other, such as New Construction Build, First Time Homebuyer, Divorce, Loan Modification, Loan Assumption, Bridge Loans, Loan Reforecasting, VA Loans, MSHDA Loans, etc. Fill out the information below, and I’ll have an experienced lender contact you.